Picture your dream retirement. You probably see a beach or a quiet cabin in the woods. Now look at your breakfast plate. Maybe it holds a bowl of bulk oats and a single boiled egg because that is all you want to spend.

This meal costs about 65 cents and lacks the beauty of an Instagram post. But for a growing group of burned out Millennials this breakfast is the most beautiful thing in the world because it buys freedom.

We are hitting peak burnout while facing historic housing costs of $427,000 and low savings. The FIRE Movement is not a daydream but a math problem that has changed significantly in 2025.

1. FIRE in 2025 The Rules Have Changed

The core idea of financial independence is simple math rather than magic or luck. You save a huge chunk of your income and keep your expenses low until the interest pays for your life.

Ten years ago this was a niche idea for software engineers but today it is a survival strategy for many people. The extreme approach is fading as we see new trends emerge that fit the economic reality of 2025 better than the old models did.

These new paths allow you to reclaim your time without having to be miserable for a decade.

- Coast FIRE means you save hard in your 20s and then stop adding money to let compound interest do the rest

- Barista FIRE allows you to leave a stress career for a part time job that covers bills and health insurance

- Lean FIRE is when you retire fully but live on a very strict budget under $40,000 a year

- The goal is to reclaim your time before you are too old to enjoy it

Coast F.I.R.E.

Save hard in your 20s, then stop adding money. Let compound interest do the rest.

Barista F.I.R.E.

Leave a stress career for a part-time job that covers bills and health insurance.

Lean F.I.R.E.

Retire fully but live on a strict budget (under $40k/year).

The Goal

Reclaim your time before you are too old to enjoy it.

2. The New Math Why 4% Is Risky

For decades the financial world treated the 4% rule as the absolute truth for retirement planning. You used to take your yearly spending and multiply it by 25 to find your freedom number.

But a 2025 Morningstar report suggests stock market valuations are too high and inflation is too sticky for that to be safe anymore.

If the market crashes right after you quit a 4% withdrawal rate could drain your account too fast so experts now suggest a safer path. You need to save more money now to ensure you do not run out of cash when you are 80.

- Morningstar now suggests a safe withdrawal rate of roughly 3.7% for 2025 retirees

- To spend $40,000 a year you used to need $1,000,000 saved under the old rules

- Under the new 3.7% rule you now need roughly $1,081,000 to have the same safety

- Sequence of Returns Risk is the danger of a market crash happening the year you retire

New Protocol

Morningstar now suggests a safe withdrawal rate of roughly 3.7% for 2025 retirees.

Target Balance

To spend $40k/year, you now need $1.08M (previously $1M under old rules) for safety.

Threat Level

Sequence of Returns Risk is the danger of a market crash happening the exact year you retire.

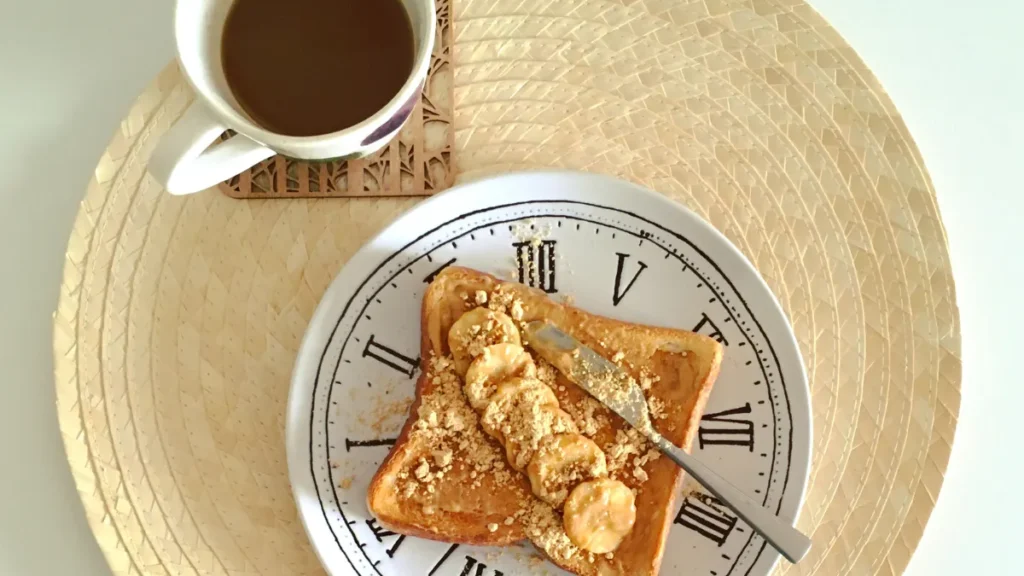

3. The $0.65 Breakfast Extreme Frugality vs Reality

We need to look at your plate to understand how gap management works in real life. To hit your savings goal you have to control the difference between what you earn and what you spend.

Grocery prices in 2025 are a shock but you can still hack the system if you are willing to eat simply. This breakfast example proves that small daily choices add up to thousands of dollars over a decade of compounding interest.

Below is the cost breakdown of a Lean FIRE breakfast compared to a standard coffee shop run.

| Item | Lean FIRE Cost | Standard Cafe Cost |

| Main Dish | $0.15 (Oats) | $12.00 (Avocado Toast) |

| Protein | $0.41 (1 Egg) | $3.00 (Add Egg) |

| Drink | $0.09 (Home Coffee) | $6.50 (Latte) |

| Daily Total | $0.65 | $21.50 |

- A single egg costs about $0.41 based on the average price of $4.95 per dozen

- Swapping a cafe brunch for a home meal saves roughly $20 every single morning

- Investing that $20 daily saving into an index fund grows massive over ten years

- The goal is not poverty but to spend money only on things that truly make you happy

Egg Cost

A single egg costs about $0.41 (based on $4.95/dozen).

Brunch Savings

Swapping a cafe brunch for home saves roughly $20 every morning.

Invest Daily

Investing that $20 daily grows massive over ten years.

The Goal

The goal is to reclaim your time before you are too old to enjoy it.

4. Increasing the Shovel Income Strategies for 2025

You cannot save your way to wealth on a small salary when rent and grocery inflation are this high. You need a bigger income shovel to fill the savings hole before you worry about cutting coupons.

The fastest way to grow your wealth in 2025 is to focus on earning more money rather than just spending less. There are three main paths people take to boost their cash flow significantly this year without waiting for a small annual raise.

- Job hopping is the fastest way to get a 15 to 20% raise by switching companies

- Skill based side hustles on platforms like Upwork pay far better than driving for Uber

- The Overemployed trend involves remote workers holding two jobs to double income instantly

- Focus on increasing income first and then apply frugality to keep the new money

Job Hopping

Switching companies is the fastest way to get a 15 to 20% raise.

Skill Stacking

Platforms like Upwork pay far better for skills than driving for Uber.

Overemployed

Remote workers holding two jobs to double income instantly.

Growth > Cuts

Focus on increasing income first, then apply frugality to keep the new money.

Where to Put the Money 2025 Investment Order?

Once you have increased your income and lowered your food costs you need a place to put the extra cash. Don’t guess where to put it because there is a specific order that maximizes your tax breaks and returns.

Following this waterfall method ensures you get every bit of free money from your employer and the government before you put cash into taxable accounts.

This system works best when you move to the next step only after filling the previous bucket.

- Your 401k match is free money so always contribute enough to get the full employer match

- The HSA is a secret weapon that offers triple tax advantages for medical costs and retirement

- A Roth IRA allows your money to grow tax free forever with a 2025 limit of $7,000

- A Brokerage Account acts as a bridge to help you retire before age 59 and a half

Free Money

Always get the full employer match in your 401k.

The Bridge

A Brokerage helps you retire before age 59½.

Tax Free

Roth IRA grows tax free forever. $7k limit (2025).

Triple Tax

HSA is a secret weapon for health & retirement.

Conclusion

FIRE is not dead but the version from 2015 where you could retire on a shoestring is gone. The math is stricter now because you need a 3.7% mindset and a higher income to outpace housing costs.

Calculate your gap number today by subtracting your spending from your income to see where you stand. That number decides if you are on track for age 65 or age 45. The $0.65 breakfast is optional but the math is mandatory.